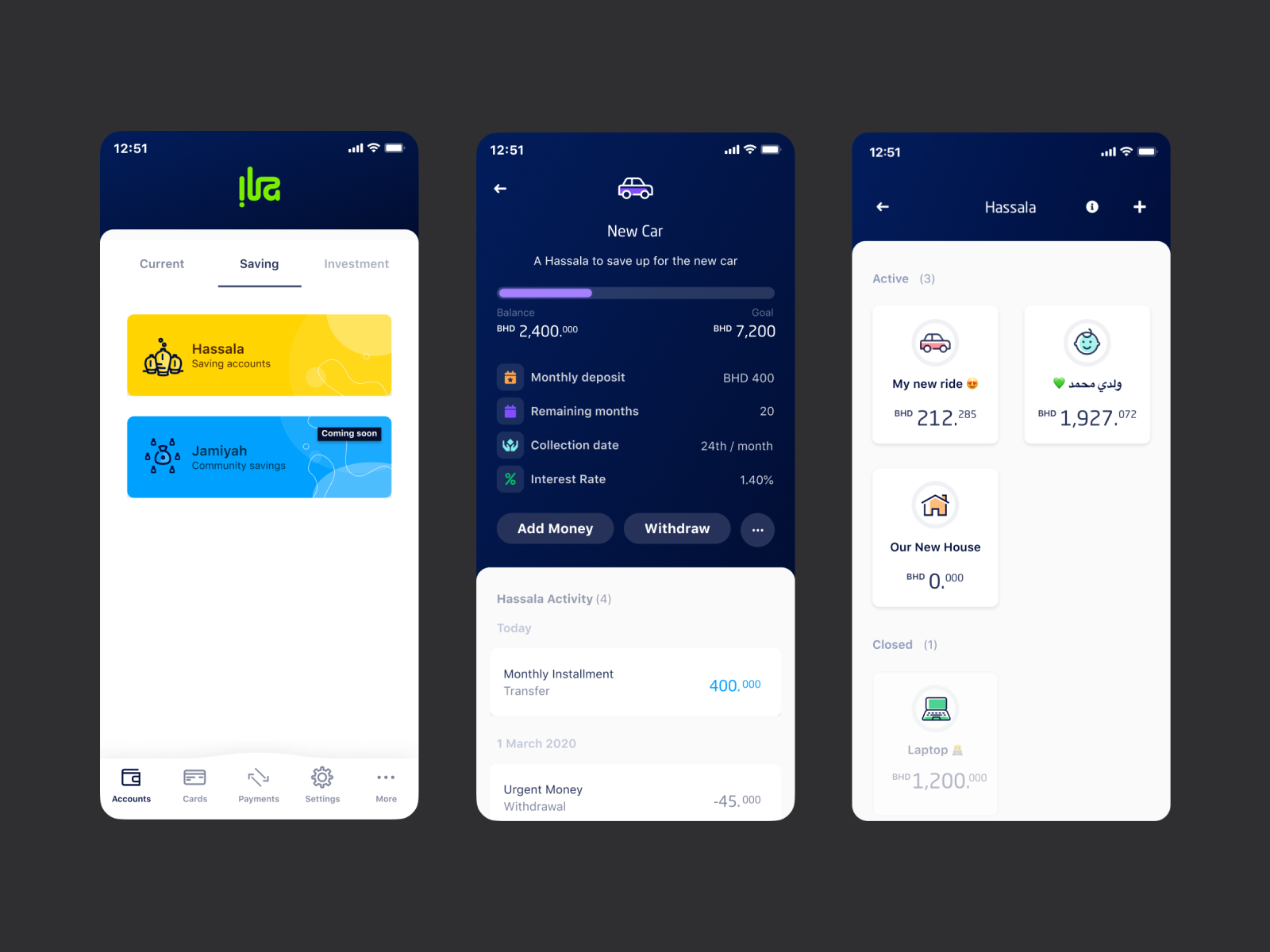

Hassala

A savings product designed for restraint, not flow — because people want their savings slightly out of reach.

Hassala is Arabic for the clay piggy bank you have to break to get into. That was the whole idea. ila Bank wanted a savings product that felt like money that reflects you, not the cold ledger of a legacy banking app — and before drawing a single screen we spent six weeks interviewing people across Bahrain about how they actually save.

Six findings came back, and the first one inverted everything a banking app is built to do.

What the research found

People deliberately make their own savings hard to reach — hiding cash, handing it to a relative, opening an account at a bank they never visit. The barrier is the product. So Hassala makes a withdrawal feel intentional and a deposit feel effortless, which is the opposite of what a current account optimises for. Around that, the research was unambiguous: savers work toward named goals and several at once, so we built pots rather than a single balance; progress is motivating, so savings show as a journey, not a number; round-ups turn spending into background saving; pay-day is the only window that reliably converts, so automatic pay-day transfers became the default. And a Sharia-compliant prize draw gave the upside that interest can’t, in a market where many decline interest on principle.

Banking apps optimise for speed by default. For savings, that optimisation actively undermines the product. Designing for restraint made the difference.

Simplifying setup

The first setup screen offered too much and cost people about thirty seconds of confusion. Three iterations later it was eight seconds in production — the work was subtraction, not addition. We coupled the deposit and duration fields so changing one recomputes the other in real time, ending the mental arithmetic. We split the locked Hassala from fixed deposits once it was clear that two things that looked alike behaved differently. And the raffle finding was too big to be a feature, so it left home: it became Al Kanz, a standalone savings experience built entirely around the prize draw.

Hassala funded more than six million dollars within ten days of launch, at a 49.9% funding rate across every pot opened. In the first month savers created 2,700 hassalas across 1,876 people — travel, cash, and a house the most common goals — and daily onboarding rose about eleven percent after launch. The product ila shipped won its share of the bank’s Red Dot and Transform MEA recognition, but the line I keep is quieter: the strongest insight was that the friction was the point.