ila Bank Cards

A card application rebuilt around who's actually applying — and controls that make trust the default.

Applying for a credit card is where a bank asks for the most trust and usually gives the least in return: a wall of terms, an opaque limit decision, and a card that arrives days later with no controls attached. For ila Bank we rebuilt the card experience from scratch — debit and credit, application through everyday management — and started, as with everything at ila, from research.

The three archetypes

The interviews surfaced three ways of relating to a card that predicted behaviour far better than any demographic. The security-conscious routed purchases through intermediaries and cared most about what could go wrong. The comparers analysed five banks before committing and wanted the numbers plain. The status-signallers cared about the card’s design as much as its rate. One application flow had to satisfy all three without three separate products.

People don’t tell you how they’ll use a card. They show you, if you ask about the last time instead of the next time.

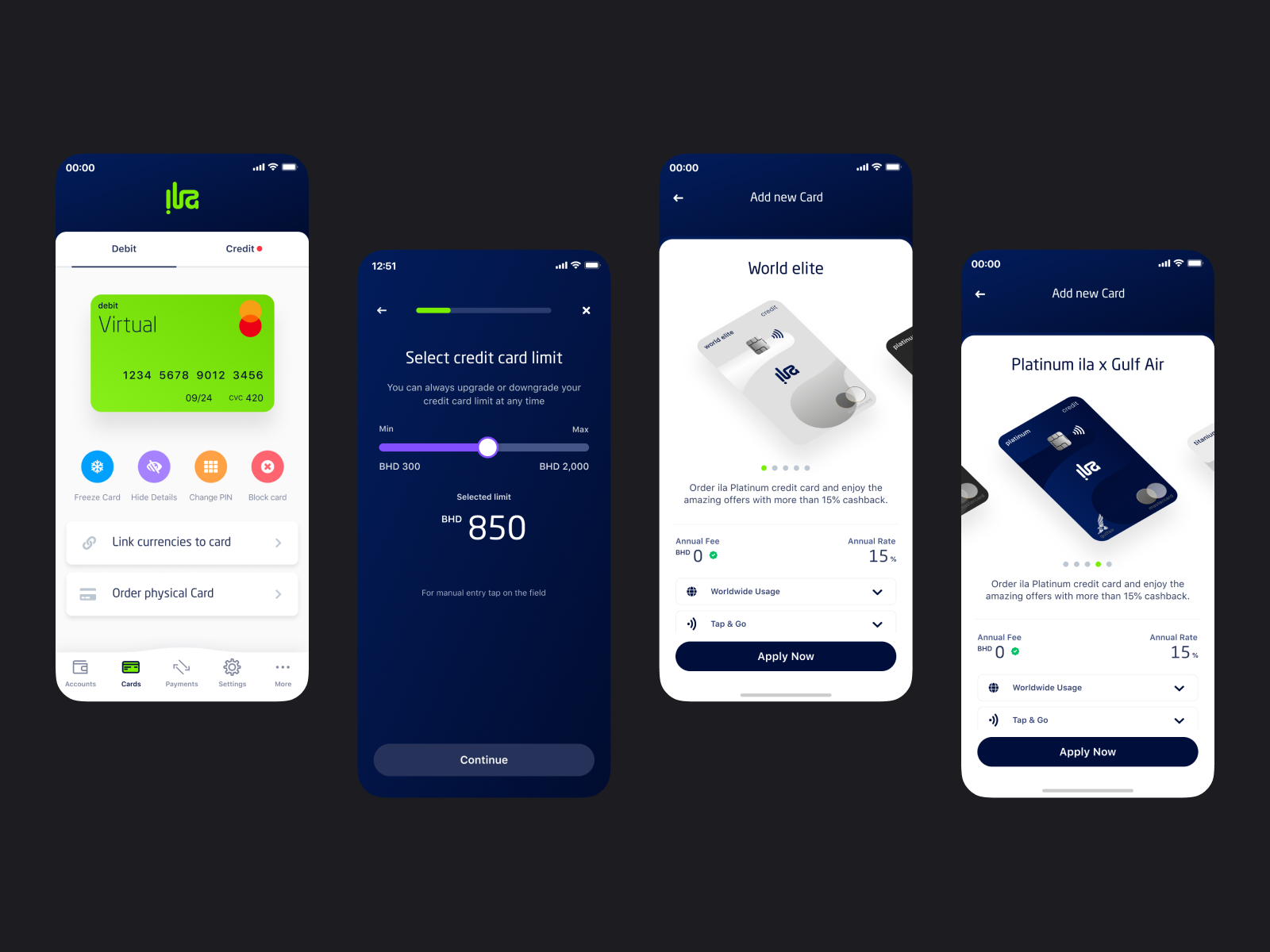

So the limit stopped being a verdict handed down after applying and became something you set — a slider from BHD 300 to 2,000, upgradeable later, with the selected figure shown large and legible while you decide. The tiers wear their value openly: a World Elite card with no annual fee and worldwide tap-and-go, and a co-branded Platinum ila × Gulf Air card for the travellers, so the status-signaller and the comparer both find what they came for on the same screen.

Card controls

The moment the card exists — as a virtual card, instantly — the controls exist with it: freeze, hide details, change PIN, block, link currencies, order the physical card. For the security-conscious user those aren’t advanced settings buried three levels deep; they’re the front page of the card, which is what turns a nervous first impression into a confident one.

Rebuilding the flow around the three archetypes meant no one was designed for at the expense of the others: the comparer gets the plain numbers, the signaller gets the card worth showing, and the cautious user gets a card they can lock before they’ve even spent on it. The application stopped feeling like a request for permission and started feeling like the first thing the card does for you.